Safe places to stash cash are earning next to nothing, so what can you do? Dividend-paying whole life insurance may be one option to consider.

It is no secret that savers are having a difficult time knowing how and where to hold their cash in this low interest rate environment.

Storing money in traditionally “safe” places no longer makes sense and has pushed some into more risky alternatives — such as fixed income securities like bonds and, in some cases even the stock market — in search of yield.

However, while fixed income securities may offer a potentially higher yield than deposit accounts, they are not a “safe” alternative for storing cash since there is potential risk of losing principal due to longevity and interest rate risk.

So the question is, what do you do when traditional methods for storing money are no longer working? There is an answer, but you must first understand two things:

1. The future is looking to be much different than the past

Looking back, we find that interest rates climbed for 40 years (early 1940s – early 1980s) then changed direction and began a steady decline for the next 30 years (early 1980s – late 2000s), when interest rates ultimately hit zero and then flatlined. This declining interest rate environment made for an ideal fixed income bull run that has since faded into a stagnant corner of the market.

2. What worked in the past may not work in the future

Fixed income experienced satisfying returns during a time of declining interest rates. However, this is no longer the case. The fact is that interest rates have no room to the downside left without going negative, and since fixed income investments like bonds have an inverse relationship to interest rates, there is no remaining upside. We have to assume that when interest rates begin rising, fixed income will eventually be negatively impacted.

The truth is that it is difficult to see how this will all play out until it is actually happening, but savers need to accept the reality that things are not what they used to be. Savers need to think outside of the box to find ways to protect their cash, take advantage of the current interest rate environment and be positioned for what happens in the future.

What you find outside of the box may surprise you

A few years back a colleague of mine asked me what I thought about the idea of using dividend-paying whole life insurance as a way to get clients higher yields on “safe money” without the interest rate risk of fixed income and without tying money up long term.

At first I dismissed the idea — like some of you may be doing right now — but the gravity of the problem made me curious enough to investigate and test the hypothesis with anticipation of finding a viable solution. Here is what I learned through my research…

Not all policies are created equal

While whole life insurance is a broadly used term for a type of permanent insurance, there are in fact many variations to choose from, leading to much of the confusion that exists about how they work.

What makes a dividend-paying whole life insurance contract different than other forms of “permanent” life insurance is its consistent growth through contract guarantees and dividends and ultimate ownership of the death benefit.

Compare these features with other forms of ”permanent” insurance and you’ll discover that a dividend-paying whole life insurance policy is arguably the only form of insurance that has the characteristics to function as a bank or bond alternative. Hybrids, such as variable, indexed, universal life or even non-participating whole life (non-participating means there are no dividends paid) have design flaws that prevent them from functioning as a viable option, and here is why:

- Variable and index contracts rely on stock market performance in determining their returns. If markets are negative or flat, the contract fees and cost of insurance can cause negative returns, making the performance unpredictable.

- A dividend-paying whole life policy, on the other hand, does not rely on stock market performance. Company guarantees and dividend tables determine the contracts’ growth, both of which are interest rate positive, which means they react favorably to rising interest rates.

- Variable, index and universal life contracts have perpetual contract fees and insurance costs that are deducted from the cash value of the contract. These can erode your equity over time.

- Meanwhile, a whole life policy has a defined funding period (usually modified at seven years) that leads to having ownership of the policy with no future cost or premiums due.

Premiums, costs and fees are the wrong conversation

Some like to debate that the death benefit of a whole life policy is too expensive compared with other forms of life insurance, leading to this paradigm that whole life insurance is a bad deal.

But I want to clarify that this is not about debating whether the death benefit is too expensive … that is the wrong conversation to be having. We are not discussing death benefits and cheap rates for coverage. We are talking about having a place to put money that can generate 3% to 4% net of costs, fees and commissions in a low interest rate environment.

If you get mentally caught up in the insurance debate you will miss the benefit of what is being discussed.

There is no perfect investment or product

The truth is that whether you put money in a bank account, the stock market or an insurance policy, there will be certain things about each of them you do not like. Maybe there is too much risk, too many fees or low returns.

Regardless of the issue, there is no perfect investment — and whole life insurance is no different. These contracts have a couple drawbacks that should be considered:

- There are premium (deposit) requirements for 5-7 years depending on the design.

- Policies have some cash restrictions in the early years that decrease over time allowing more access each year that passes. (In year one, 65%-80% access to cash and increasing to 100% by years 8-10 years depending on the design.)

But knowing this to be true, we have to weigh the negatives with the positives and then consider the alternatives.

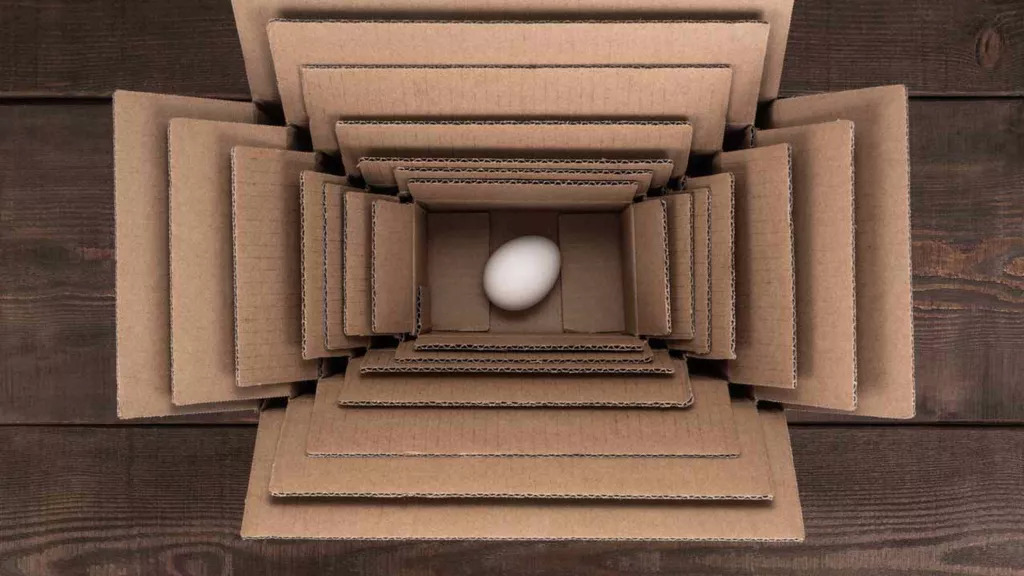

Here is a quick comparison of popular options for storing money to highlight the attributes of each of them side by side:

When you evaluate the three options, you find:

- A low interest deposit account paying close to zero.

- A fixed income option paying below 3% with volatility, tax liabilities and with interest rate risk.

- A dividend-paying whole life insurance contract with consistent growth of 3% to 4%, not subject to market risk, tax-free growth and access to cash.

Clearly not a unicorn, but when comparing the attributes of these contracts to deposit and fixed income accounts, whole life insurance does prove to be a “best” option.

Conclusion

I have been in the financial planning business for nearly three decades and have had my own personal roller coaster relationship with life insurance over the years. It wasn’t until I was challenged to set my personal biases and opinions aside to look at the facts that I able to see the possibilities of using specially designed life insurance.

The truth is that most of what you hear or read about whole life insurance are repeated thoughts and opinions from one person to another with little if any testing or vetting of the facts.

Knowing the facts and avoiding too much opinion when making decisions will help you navigate these decisions and lead you to the answer you are looking for.

For more, please see my podcasts: Life Insurance as a Bank Alternative and Life Insurance as an Asset Class.